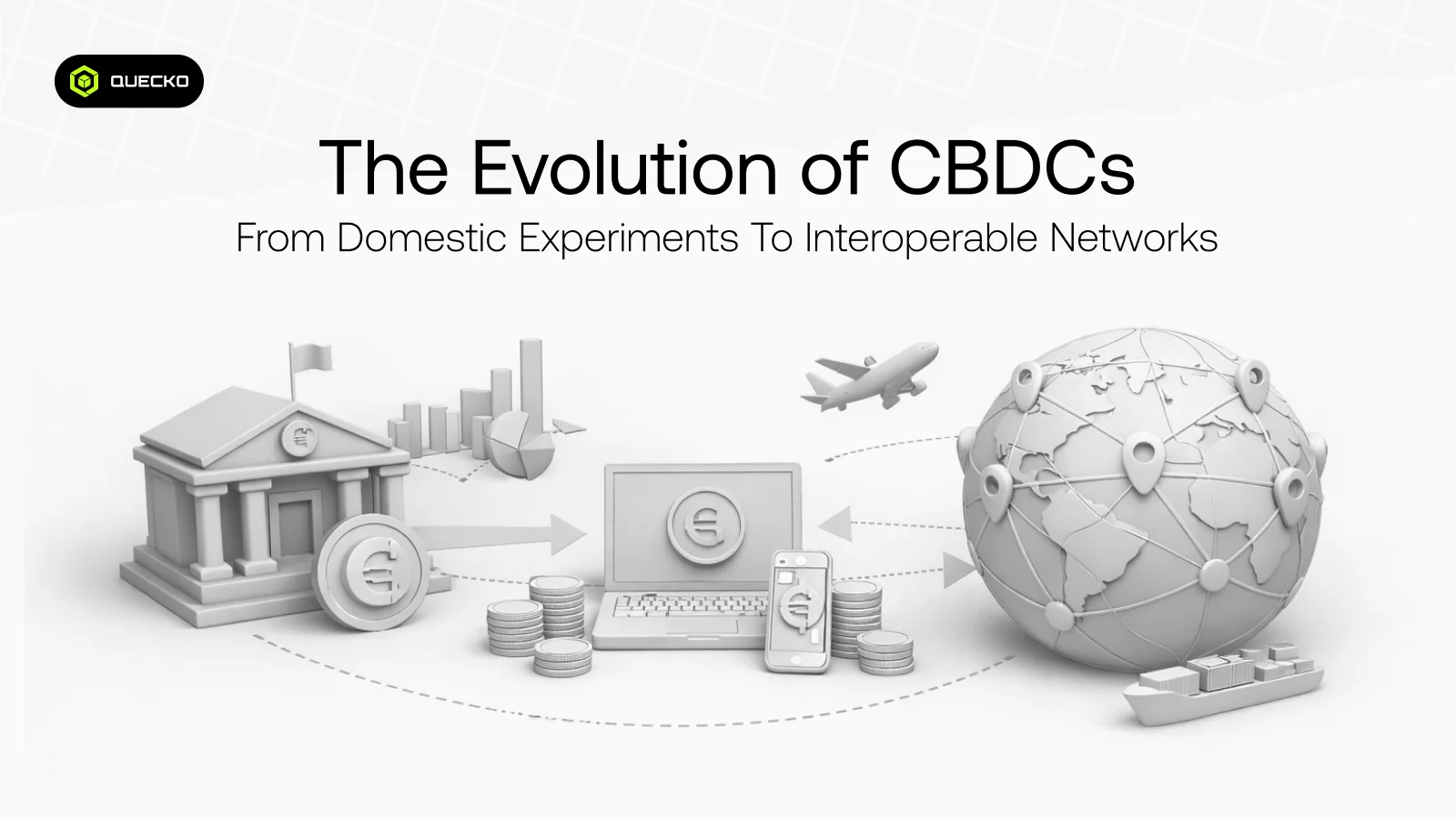

The Evolution of CBDCs: From Domestic Experiments to Interoperable Networks

Explore the evolution of CBDCs, from domestic pilots to interoperable networks, and learn how digital currencies reshape payments, policy, and global finance.

Central Bank Digital Currency (CBDC) is not merely a concept discussed in academic publications and political discussion forums. Central banks across the globe are considering digital money as a new type of fiat currency, one that exists purely in digital form yet is backed by the power of the state. Any of these attempts is shaping the future of digital currencies, re-defining Digital Payments, and altering the way economies think about Financial Inclusion, Fintech Rails, and International Payments.

The paper provides a precise, non-technical explanation of the development of CBDCs over time: from the first experiments in national jurisdictions to the present-day trend of cross-chain interoperability and international networks connecting countries, institutions, and financial systems.

What Is a Central Bank Digital Currency?

Central Bank Digital Currency (CBDC) is no longer a fantasy discussed in academic publications and policy forums. Digital money is a new type of fiat currency that central banks across countries are considering, but it exists in a fully digital format and is backed by the state. Any of these undertakings is shaping the future of digital currencies, redefining Digital Payments and transforming how economies think about Financial Inclusion and International Payments.

The paper provides a precise, non-technical explanation of the development of CBDCs over time: from the first experiments in national jurisdictions to the present-day trend of cross-chain interoperability and international networks connecting countries, institutions, and financial systems.

CBDCs are designed to support:

- Safer Digital Payments

- More efficient cross-border settlement

- Stronger Privacy Protections

- Better Monetary Policy Transmission

Why Governments and Central Banks Are Exploring CBDCs

The emergence of electronic currencies and commercial payment systems has threatened the ancient position of central banks. Institutions such as the International Monetary Fund, the Financial Stability Board, and the Federal Reserve Board are studying how CBDCs can support economic stability, enhance Payment Resilience, and modernize financial infrastructure. Some of the main goals include:

Financial Inclusion

CBDCs can give people without access to traditional banking a way to store and transfer digital money using just a mobile phone and a digital identity. This supports broader access to financial services and promotes Open Access to the digital economy.

Faster and Cheaper Payments

By improving payment rails and integrating with Universal Payment Channel systems, CBDCs can reduce delays and costs in both domestic and cross-border payments.

Stronger Regulatory Oversight

CBDCs allow governments to design a clear regulatory framework and Legal Framework rules around AML/CFT Standards, helping prevent fraud, money laundering, and financial crime while maintaining the Rule of law.

The Technology Behind CBDCs

Behind every CBDC is a carefully designed digital infrastructure that combines secure networks, cryptography, and shared ledgers to ensure money can move safely, transparently, and efficiently in a fully digital environment.

Distributed Ledger Technology

The majority of CBDC systems are developed using Distributed Ledger Technology. This technology enables two or more trusted parties to maintain a common, unaltered record of transactions.

Rather than consolidating all of the data in the database, the transactions are stored in a network of systems, thereby forming what some developers refer to as an on-chain golden record, or a single, provable source of truth.

Permissioned Chains vs Public Blockchains

Some CBDCs are based on permissioned chains (as opposed to cryptocurrencies operating on public blockchains). It implies that transactions will only be validated by approved institutions, including central banks and licensed financial providers. The design will prioritize superior cybersecurity protection, compliance with national legislation, and Privacy Protections.

Retail CBDCs vs Wholesale CBDCs

CBDCs are designed for different users and purposes, with some focused on everyday public use and others built to power high-value transactions between banks and financial institutions.

Retail CBDCs

Retail CBDCs are designed for everyday users, citizens, and businesses. They are used for shopping, bill payments, peer-to-peer transfers, and savings. These systems often integrate with:

- digital wallets

- QR payments

- instant payments systems

The goal is to make Digital currency electronic payment as simple and reliable as using cash or a debit card.

Wholesale CBDCs

Wholesale CBDCs are designed for financial institutions rather than the public. Banks use them for large-value transactions, securities settlement, and cross-border settlement. These systems aim to improve efficiency, reduce risk, and strengthen Payment Resilience across the financial system.

Early Domestic CBDC Experiments

Many countries started with small-scale CBDC experiments to test how Digital Payments and Digital identity systems would work in real-world conditions.

Project Hamilton

Project Hamilton explored high-performance transaction systems for retail CBDCs, focusing on speed, security, and system scalability.

Digital Dollar Project and Tokenized Digital Dollar

The Digital Dollar Project and research into a Tokenized Digital Dollar examined how a U.S. CBDC could support modern payment systems, financial stability, and Monetary Policy Transmission.

Digital Currency Initiative

On the topic of blockchain networks supporting national digital currencies, the Digital Currency Initiative has funded research on blockchain-based financial systems and assisted policymakers in understanding their potential.

Domestic pilots made governments aware of user behavior, energy usage, system security, transparency, and Privacy Protection.

Moving Toward Cross-Border CBDC Networks

The globalization of trade and commerce is leading countries to realize that isolated CBDC systems are insufficient. The second step is on cross-border CBDC projects and cross-chain interoperability.

Project Dunbar

Project Dunbar examined the possibility of using a common platform to enable cross-border payments and settlements across multiple countries, thereby reducing costs and time delays in international transfers.

Project Jura

Project Jura tested wholesale CBDCs for international securities transactions, demonstrating how Distributed Ledger Technology can securely connect different financial systems.

Project Cedar

Project Cedar was dedicated to enhancing the infrastructure for international wholesale transactions, improving Payment Resilience, and the system’s reliability.

These projects are designed to establish a common payment channel that would allow national digital currencies to flow freely across borders without violating each country’s regulatory framework.

Governance, Law, and Global Cooperation

CBDCs are not purely technical projects; they are also legal and political projects. Governments should develop effective legal frameworks to specify how data is stored, how disputes are resolved, and how data is protected.

International organizations such as the International Monetary Fund and the Financial Stability Board set international standards, while domestic policy is formulated by national institutions such as the Federal Reserve Board.

Key considerations include:

- AML/CFT Standards

- Data privacy and IP Address protection

- User support systems and support team processes

- Licensing and intellectual property rules, including the Creative Commons Attribution-NonCommercial-NoDerivs licence for research and public resources

Security and Cyber Resilience

As CBDCs become part of the national infrastructure, they become potential targets for cyber attacks. That’s why cybersecurity safeguards and strong Payment Resilience strategies are critical.

Systems must be able to:

- Recover quickly from technical failures

- Protect sensitive user data

- Prevent fraud and unauthorized access

A strong on-chain golden record and secure Distributed Ledger Technology design help maintain trust and system integrity.

The Role of Research Institutions and Experts

CBDC design and policy are significantly influenced by academic and industry professionals. Research on system security, governance, and interoperability is conducted at institutions such as the Edinburgh Blockchain Lab and the UCL Lab of Blockchain Technologies.

Some of the most active contributors include Professor Aggelos Kiayias, Dr Geoffrey Goodell, Pavle Avramovic, and Dr Giovanni Bassani, who have discussed how blockchain-based systems could balance innovation, compliance, privacy, and public trust.

CBDC Adoption and the Digital Economy

For CBDCs to succeed, CBDC Adoption must be supported by strong infrastructure, user education, and integration with existing Digital Payments systems.

Governments are also linking CBDCs to broader Digital Economy Agreements that define how data, money, and services flow across borders. This connects financial innovation with global trade, geopolitical power, and long-term economic strategy.

The Future

The long-term vision for CBDCs is a world where national digital currencies can move across borders as easily as emails. Through cross-chain interoperability, shared payment rails, and aligned regulatory framework rules, CBDCs could form a global network of trusted digital money systems.

This future promises:

- Faster international trade

- Lower transaction costs

- Stronger Financial Inclusion

- Greater transparency and trust

Conclusion

A significant transformation in how the world perceives money is the development of CBDCs, which began as small domestic experiments but are now large-scale, interoperable networks worldwide. Through the integration of Distributed Ledger Technology, well-developed legal and regulatory systems, and international collaboration, central banks are setting the stage for another Digital fiat money age.

As retail CBDCs and wholesale CBDCs continue to develop, and as projects like Project Dunbar, Project Jura, and Project Cedar push the boundaries of cross-border payments, the vision of a truly connected, resilient, and inclusive digital financial system is becoming increasingly real.

Author

Fatima Ahmed

No description availableDate

4 months agoShare on

+971-50-740-0268

+971-50-740-0268